Materiality Assessment

In FY2025, we conducted a double materiality assessment at the Group level1 to identify and prioritise sustainability-related risks and opportunities, aligning with both the GRI Standards 2021 and the IFRS S1 requirements on materiality. Compared to the previous assessment we have done in 2017 and subsequent refreshment in 2022, which focused on the impact of sustainability topics on the company and its stakeholders, this year's assessment incorporated an additional financial materiality lens, considering the potential influence of sustainability-related matters on enterprise value.

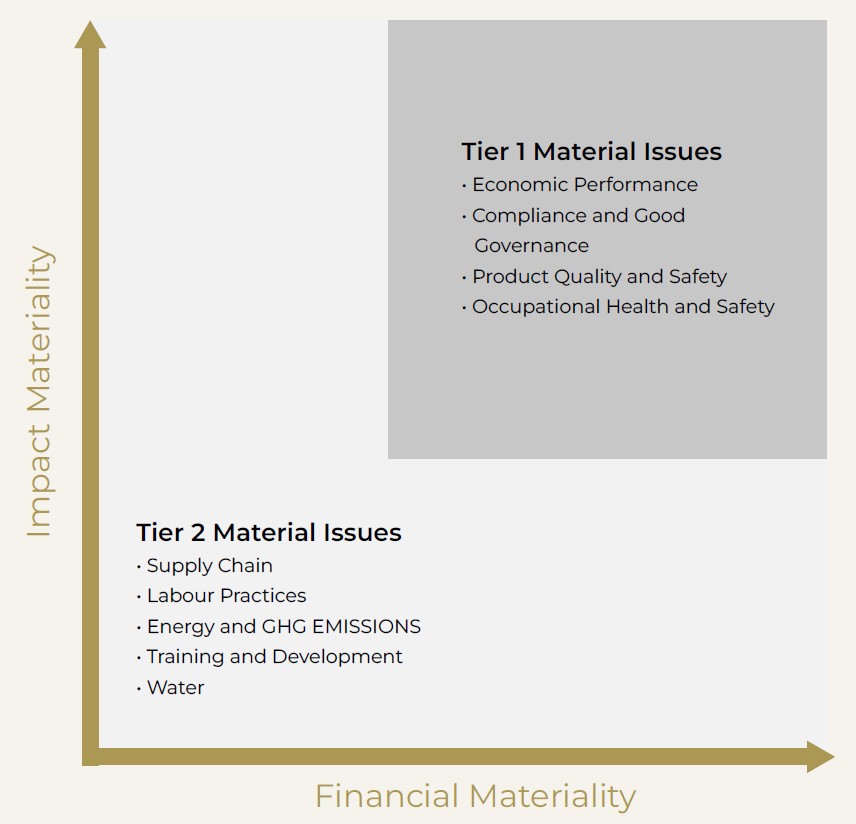

Through this process, nine (9) material topics were identified for FY2025 and subsequently prioritised into Tier 1 and Tier 2 topics, as illustrated below.

Haw Par's materiality matrix